"Whenever legislators endeavor to take away and destroy the property of the people, or to reduce them to slavery under arbitrary power, they put themselves into a state of war with the people, who are thereupon absolved from any further obedience."

- - John Locke, 1690

"When the government fears the people, you have liberty. When the people fear the government [or the IRS, for that matter], you have tyranny."

(Thomas Jefferson, author of the Constitution of the United States)

"Better is a little with righteousness. Than vast revenues without justice." (Bible, Prov. 16:8-9)

Subject: IRS Abuses Regarding Rights of Information and Actions

This covers the following sections of Title 26 Internal Revenue Laws, hereafter referred to as such, or as the

IRC:

Item: Section: Title: Page:

1 6001 Notice or regulations requiring records, statements, and special returns 1

2 6011 General requirement of return, statement, or list 2

3 6012 General requirement of return, statement, or list 8

4 6020 Returns prepared for or executed by Secretary 9

5 6201 Assessment authority 10

6 6203 Method of assessment 10

7 6301 Collection authority 12

8 6321 Lien for tax 12

9 6331 Levy and distraint 13

10 6682 False information with respect to withholding 14

11 7608 Authority of internal revenue enforcement officers 15

-- 6343 Authority to release levy and return property 16

-- 7214 Offenses by officers and employees of the United States 16

In regards to all following the provisions of Title 5--Government Organization and Employees, Part I--The

Agencies Generally, Chapter 5--Administrative Procedure, Subchapter II--Administrative Procedure apply as

recognized in 26 CFR § 601.702 Publication and public inspection.

1. Title 26 (IRC) Section 6001: Notice or regulations requiring records, statements, and special returns.

The IRS uses the statement "Our legal right to ask for information is Internal Revenue Code sections

6001. 6011 and 6012(b) and their regulations. They say that you must file a return or statement with us

for any tax you are liable for. Your response is mandatory under these sections. Code section 6109

requires that you provide your social security number or individual taxpayer identification number on what

you file."

[6109 brings up yet another matter. 6109 and its regulations require taxpayers to obtain taxpayer numbers for

income tax purposes, and employers and individual employees to obtain numbers for employment tax

purposes. Thus, having been directed to 6109, we learn that the W-4 Privacy Act Statement, which Act

requires Agencies to state why they are asking for the information, is really telling us that Social Security

Numbers and Employer ID numbers are for employment taxes, and taxpayer numbers for income

taxes, which are entirely different things, and are used for entirely different purposes by entirely different

classes of "taxpayers". Taxpayer numbers are for withholding agents and nonresident aliens, and

employment numbers are for government employees and their benefit programs.]

Emphasis is placed on the words "and their regulations" as it indicates that the IRS is well aware that

enforcement of the code sections is by the regulations that are implemented for them and entered in the

Federal Register. It is only those regulations so entered and having final rule (regulation) status that have

legal effect.

6001 makes the statement "Every person liable for any tax imposed by this title, or for the collection

thereof, shall keep such records, render such statements, make such returns, and comply with such rules

and regulations as the Secretary may from time to time prescribe" without identifying the taxes addressed

by this section. Since enforcement of a section is dependent upon regulations it is the regulations for this

section that identify the taxes concerned. Pertinent facts in regards to these parts/sections in Title 26 CFR

are shown in the following recap. Since 26 CFR Parts 55 (Excise tax on real estate investment trusts and

regulated investment companies) and 156 (Excise tax on greenmail) do not apply to most they are

omitted from listing:

CFR Part/Sec Facts

1.6001-1 Applies to Subtitle A source document giving regulatory (rule) authority of law:

T.D. 6500, 25 FR 12108, Nov. 26, 1960, as amended by T.D. 7122, 36 FR 11025,

June 8, 1971; T.D. 7577, 43 FR 59357, Dec. 20, 1978; T.D. 8308, 55 FR 35593,

Aug. 31, 1990

1.6001-2 Refers to returns required to be made by every individual, estate, or trust which is

liable for one or more qualified State individual income taxes (T.D. 6516, 25 FR

13032, Dec. 20, 1960, T.D. 7577, 43 FR 59357, Dec. 20, 1978)

31.6001-1 General – no authorizing regulations. Refers to Sec’s. 31.6001-2 to 31.6001-5,

inclusive, for additional records required with respect to the Federal Insurance

Contributions Act, the Railroad Retirement Tax Act, the Federal Unemployment

Tax act, and the collection of income tax at source on wages.

31.6001-2 Refers to every employer liable for tax under the Federal Insurance Contributions

Act (T.D. 6516, 25 FR 13032, Dec. 20, 1960, T.D. 7001, 34 FR 1003, Jan. 23,

1969)

31.6001-3 General – no authorizing regulations. Refers to every employer liable for tax

under the Railroad Retirement Tax Act

31.6001-4 Refers to Every employer liable for tax under the Federal Unemployment Tax Act

(T.D. 6516, 25 FR 13032, Dec. 20, 1960, T.D. 6658, 28 FR 6642, June 27, 1963)

31.6001-5 Refers to every employer required under section 3402 to deduct and withhold

income tax upon the wages of employees shall keep records of all remuneration

paid to (including tips reported by) such employees (T.D. 6516, 25 FR 13032,

Dec. 20, 1960, T.D. 6606, 27 FR 8516, Aug. 25, 1962)

31.6001-6 General – no authorizing regulations.

In regards to the above regulations from 26 CFR Part 1 Income Tax it is noted that 26 CFR 601.101(a)

states that "The Internal Revenue Service is the agency by which these functions are performed. Within

an internal revenue district, the internal revenue laws are administered by a district director of internal

revenue. The Director, Foreign Operations District, administers the internal revenue laws applicable

to taxpayers residing or doing business abroad, foreign taxpayers deriving income from sources

within the United States, and taxpayers who are required to withhold tax on certain payments to

nonresident aliens and foreign corporations, provided the books and records of those taxpayers

are located outside the United States."

Notice that these regulations therefore apply only to the internal revenue laws applicable to taxpayers

residing or doing business abroad, foreign taxpayers deriving income from sources within the United

States, and taxpayers who are required to withhold tax on certain payments to nonresident aliens and

foreign corporations. Further referral could be made to 26 section 1461 and sections 1441 through 1443.

Those indicated in 26 Part 31 (Employment taxes and collection of income tax at source) apply to the

titles and subject matter as shown above. Since these requirements are applicable to "employers", they

again do not apply to an individual who is not an "employer" within the meaning of the term as defined.

Further, regulations for 26 USC section 6001 also exist in 27 CFR Parts 19, 53, 194, 250, and 296. These

sections relate to Distilled spirits plants, Manufacturers excise taxes--firearms and ammunition, Liquor

dealers, Liquors and articles from Puerto Rico and the Virgin Islands, and Miscellaneous regulations

relating to tobacco products and cigarette papers and tube respectively. These 27 CFR regulations are

only applicable to alcohol, tobacco, and firearm related activities.

2. Title 26 (IRC) Section. 6011. General requirement of return, statement, or list

This section pertains to the requirement to furnish a return. In 6011(a) the very first sentence reads,

"When required by regulations prescribed by the Secretary any person made liable for any tax imposed

by this title, or with respect to the collection thereof, shall make a return or statement according to the

forms and regulations prescribed by the Secretary." Since it states, "required by regulations" it is again

evidence of the fact that the IRS is aware that enforcement relies on regulations. These regulations

for IRC section 6011 are as follows. Since 26 CFR Parts 40 (Excise tax procedural regulations), 55 (Excise

tax on real estate investment trusts and regulated investment companies) and 156 (Excise tax on

greenmail) do not apply to most they are not listed.

CFR Part/Sec Title

31.6011(a)-1 Returns under Federal Insurance Contributions Act - Forms 941, 942, 943A,

943PR, W-2, 941VI, 941c, 941cPR, 1040, 1040SS, 1040PR (T.D. 6516, 25 FR

13032, Dec. 20, 1960, as amended by T.D. 7001, 34 FR 1004, Jan. 23, 1969; T.D.

7001, 34 FR 1826, Feb. 7, 1969; T.D. 7200, 37 FR 16544, Aug. 16, 1972; T.D.

7351, 40 FR 17144, Apr. 17, 1975; T.D. 7396, 41 FR 1903, Jan. 13, 1976)

31.6011(a)-2 Returns under Railroad Retirement Tax Act – Forms CT-1, CT-2 (T.D. 6516, 25 FR

13032, Dec. 20, 1960; 25 FR 14021, Dec. 31, 1960, as amended by T.D. 7396, 41

FR 1903, Jan. 13, 1976)

31.6011(a)-3 Returns under Federal Unemployment Tax Act – Form 940 (T.D. 6516, 25 FR

13032, Dec. 20, 1960, as amended by T.D. 7200, 37 FR 16544, Aug. 16, 1972)

31.6011(a)-3A Returns of the railroad unemployment repayment tax - Form 940 (T.D. 8105, 51

FR 40168, Nov. 5, 1986. Redesignated and amended at T.D. 8227, 53 FR 34736,

Sept. 8, 1988)

31.6011(a)-4 Returns of income tax withheld – Forms 941, 942, 943, 945 (T.D. 6516, 25 FR

13032, Dec. 20, 1960, as amended by T.D. 7096, 36 FR 5217, Mar. 18, 1971; T.D.

7200, 37 FR 16544, Aug. 16, 1972; T.D. 7577, 43 FR 59359, Dec. 20, 1978; T.D.

7580, 43 FR 60159, Dec 26, 1978; T.D. 8504, 58 FR 68035, Dec. 23, 1993; T.D.

8624, 60 FR 53510, Oct. 16, 1995; T.D. 8672, 61 FR 27008, May 30, 1996)

31.6011(a)-5 Monthly returns - Forms 941, 941PR, 941VI, 945, W-3, W-2 (T.D. 6516, 25 FR

13032, Dec. 20, 1960; 25 FR 14021, Dec. 31, 1960, as amended by T.D. 7351, 40

FR 17145, Apr. 17, 1975; T.D. 7580, 43 FR 60154, Dec. 26, 1978; T.D. 8637, 60

FR 66133, Dec. 21, 1995)

31.6011(a)-6 Final returns - Forms 940, 942, 943, CT-1, CT-2 (T.D. 6516, 25 FR 13032, Dec.

20, 1960; 25 FR 14021, Dec. 31, 1960, as amended by T.D. 7396, 41 FR 1904,

Jan. 14, 1976; T.D. 8637, 60 FR 66133, Dec. 21, 1995)

31.6011(a)-7 Execution of returns - Form W-2 (T.D. 6516, 25 FR 13032, Dec. 20, 1960, as

amended by T.D. 6606, 27 FR 8516, Aug. 25, 1962; T.D. 6883, 31 FR 6590, May

3, 1966; T.D. 7276, 38 FR 11345, May 7, 1973; T.D. 7396, 41 FR 1904, Jan. 13,

1976; T.D. 7580, 43 FR 60159, Dec. 26, 1978)

31.6011(a)-8 Composite return in lieu of specified form ([T.D. 7200, 37 FR 16544, Aug. 16,

1972)

31.6011(a)-9 Instructions to forms control as to which form is to be used (T.D. 7351, 40 FR

17145, Apr. 17, 1975)

31.6011(b)-1 Employers' identification numbers (T.D. 6516, 25 FR 13032, Dec. 20, 1960, as

amended by T.D. 6606, 27 FR 8517, Aug. 25, 1962; T.D. 7012, 34 FR 7693, May

15, 1969)

31.6011(b)-2 Employees' account numbers (T.D. 6516, 25 FR 13032, Dec. 20, 1960, as

amended by T.D. 6606, 27 FR 8517, Aug. 25, 1962)

From the above it is shown that the requirements are those of an "employer" by fact of the forms

prescribed. In this regard a look at the Form 941 needs to be done, it has an OMB Number of 1545-0029

and is governed by the regulations shown below::

Regulation: Title/Contents:

31.3102-3 Collection of, and liability for, employee tax on tips.

31.3121(b)(19)-1 Services of certain nonresident aliens.

31.3121(r)-1 Election of coverage by religious orders.

31.3121(s)-1 Concurrent employment by related corporations with common paymaster.

31.3306(c)(18)-1 Services of certain nonresident aliens.

31.3401(a)(6)-1 Remuneration for services of nonresident alien individuals.

31.3401(a)(7)-1 Remuneration paid before January 1, 1967, for services formed by

nonresident alien individuals who are residents of a contiguous country and

who enter and leave the United States at frequent intervals.

31.3401(a)(8)(A)-1 Remuneration for services performed outside the United States by citizens

of the United States.

31.3401(a)(8)(C)-1

Remuneration for services performed in Puerto Rico by citizen of the United States.

31.3401(a)-1 Wages.

31.3402(h)(1)-1 Withholding on basis of average wages.

31.3402(h)(3)-1 Withholding on basis of cumulative wages.

31.3404-1 Return and payment by governmental employer.

31.3504-1 Acts to be performed by agents.

31.6001-6 Notice by district director requiring returns, statements, or the keeping of

records.

31.6011(a)-1 Returns under Federal Insurance Contributions Act.

31.6011(b)-2 Employees' account numbers.

31.6053-1 Report of tips by employee to employer.

31.6065(a)-1 Verification of returns or other documents.

31.6071(a)-1 Time for filing returns and other documents.

31.6091-1 Place for filing returns.

31.6205-1 Adjustments of underpayments.

31.6413(a)-1 Repayment by employer of tax erroneously collected from employee.

31.6413(a)-2 Adjustment of overpayments.

31.6413(c)-1 Repayment by payor of tax erroneously collected from payee.

31.6414-1 Credit or refund of income tax withheld from wages.

32.1 Social security taxes with respect to payments on account of sickness or

accident disability.

32.2 Railroad retirement taxes with respect to payments on account of sickness

or accident disability.

36.3121(1)(10)-1 Requirements in respect of liability under agreement.

36.3121(1)(10)-3 Returns.

301.6316-7 Payment of Federal Insurance Contributions Act taxes in foreign currency.

In the above, Part 36 is in regards to Contract coverage of employees of foreign subsidiaries. Remember

that 26 CFR Part 601.101(a) included the wording "internal revenue laws applicable to taxpayers residing

or doing business abroad, foreign taxpayers deriving income from sources within the United States, and

taxpayers who are required to withhold tax on certain payments to nonresident aliens and foreign

corporations, provided the books and records of those taxpayers are located outside the United States."

Therefore, from the list of regulations to be used in completing the form it is readily apparent that

31.3121(b)(19)-1, 31.3306(c)(18)-1, 31.3401(a)(6)-1, and 31.3401(a)(7)-1 are applicable to foreign

taxpayers deriving income from sources within the United States, and taxpayers who are required to

withhold tax on certain payments to nonresident aliens and foreign corporations.

By the same reasoning, 26 CFR Part 601.101(a) included the wording "internal revenue laws applicable to

taxpayers residing or doing business abroad". Therefore regulations 31.3401(a)(8)(A)-1 and

31.3401(a)(8)(C)-1 would be applicable. Since 31.3401(a)(8)(A)-1 relates only to services performed

outside the United States by citizens of the United States it is not applicable to those citizens residing in

the 50 State Republics and not doing business abroad.

The following statement appears in the instructions for completing the Form 941:

Line 2— Total wages and tips plus other compensation

Enter the total of all wages paid, tips reported, taxable

fringe benefits provided, and other compensation paid to

your employees, even if you do not have to withhold

income or social security and Medicare taxes on it.

Do not include supplemental unemployment

compensation benefits, even if you withheld income tax

on them. Do not include contributions to employee plans

that are excluded from the employee's wages (e.g.,

section 401(k) and 125 plans). [emphasis added]

The wording "even if you do not have to withhold income or social security and Medicare taxes on it"

indicates that not all pay is subject to withholding and social security/Medicare taxes are not necessarily

mandatory.

Since the above is in regards to the term "wages" a look at the appropriate regulations as listed is called

for. Since wages subject to withholding under chapters 21, 22, 23, and 24 of the IRC are included in the

regulations specified for these forms a closer look at the IRC sections and their regulations are in order.

For purposes of brevity, and because the RRTA withholding of chapter 22 is similar to that of FICA in

chapter 21 (only applies to a specific group) we can narrow what needs to be looked at to those

regarding FICA (chapter 21) and withholding at source on wages (chapter 24). Chapter 23 is in regards

to the Federal Unemployment Tax Act and regards employers only so will not be covered.

In regards to this, a look at IRC section 3121(a) which defines "wages" in regards to chapter 21 is in

order. In doing so it is evident that it contains many words which makes for "fuzzy interpretation. The

statement "(as determined under section 230 of the Social Security Act)" is of significance though. By

referring to the "References in Text" section of IRC section 3121 the following is stated:

REFERENCES IN TEXT

The Social Security Act, referred to in subsecs. (a)(1), (15), (b), (d)(4), (j)(2)(D), (4)(B), (l)(1), (4), (6),

(r)(3)(A), (u), (w)(1), and (x), is act Aug. 14, 1935, ch. 531, 49 Stat. 620, as amended. Title II of the Act

is classified generally to subchapter II (Sec. 401 et seq.) of chapter 7 of Title 42, The Public Health

and Welfare. Sections 201, 210, 215, 218, 223, 230, and 233 of the Act are classified to sections

401, 410, 415, 418, 423, 430, and 433, respectively, of Title 42. For complete classification of this Act

to the Code, see section 1305 of Title 42 and Tables.

We find that Title II of the act is classified generally to subchapter II (Sec. 401 et seq.) of chapter 7 of Title

42 and that certain sections of the Act are classified to the sections of Title 42, chapter 7 as shown in the

following:

Title II Act Sections Title 42 Sections

201 401

210 410

215 415

218 418

223 423

230 430

233 433

So as it was stated in IRC 3121 "as determined under section 230 of the Social Security Act" we need to

see what section 230 of the act as codified in Title 42 Section 430 states:

Sec. 430. Adjustment of contribution and benefit base

(c) Amount of base for period prior to initial cost-of-living benefit increase

For purposes of this section, and for purposes of determining wages and self-employment income under sections 409, 411, 413, and 415 of this title and sections 1402, 3121, 3122, 3125, 6413, and 6654 of the Internal Revenue Code of 1986, … ..

Section Referred to in Other Sections

This section is referred to in sections 403, 409, 411, 413, 415 of

this title; title 5 section 8334; title 26 sections 401, 936, 1402,

3121, 3231, 6413; title 29 section 1322.

In looking at it we note that it states "for purposes of determining wages and self-employment income under

sections 409, 411, 413, and 415 of this title and sections 1402, 3121, 3122, 3125, 6413, and 6654 of the

Internal Revenue Code of 1986".

Therefore to determine what constitutes "wages" we need to refer to sections 409, 411, 413, and 415 of

Title 42. It is Title 42, section 409 that defines "wages. In section 409(b), Regulations providing exclusions

from term the following is stated: "Nothing in the regulations prescribed for purposes of chapter 24 of

the Internal Revenue Code of 1986 (relating to income tax withholding) which provides an

exclusion from "wages'' as used in such chapter shall be construed to require a similar exclusion

from "wages'' in the regulations prescribed for purposes of this subchapter."

Notice where it states that if an exclusion exists for purposes of chapter 24 of the Internal Revenue Code

of 1986 (relating to income tax withholding) will also apply to this subchapter (Subchapter II--Federal Old-

Age, Survivors, and Disability Insurance). At this point, a look at the regulations for IRC section 3121 and

Title 42 section 409 and applicable Federal Register entries should be made.

Since 26 CFR Part 31 covers Employment taxes and collection of income tax at source it is found that

31.3121(a)-1 concerns the definition of "wages" and makes reference to section 230 of the Social

Security Act for determining maximum amounts of remuneration subject to withholding. An entry in the

Federal Register at T.D. 6516, 25 FR 13032, Dec. 20, 1960 lists the different sections/subsections of

3121 and states that all employment tax regulations pursuant to the Internal Revenue Code of 1954 are

entered as republished for purposes of editorial changes and corrections of form, style, and internal

references.

Since section 230 of the Social Security Act is referenced and that is codified in Title 42 section 409 a

look at the regulations for that section is in order. The regulations are found at 20 CFR Part 404. By

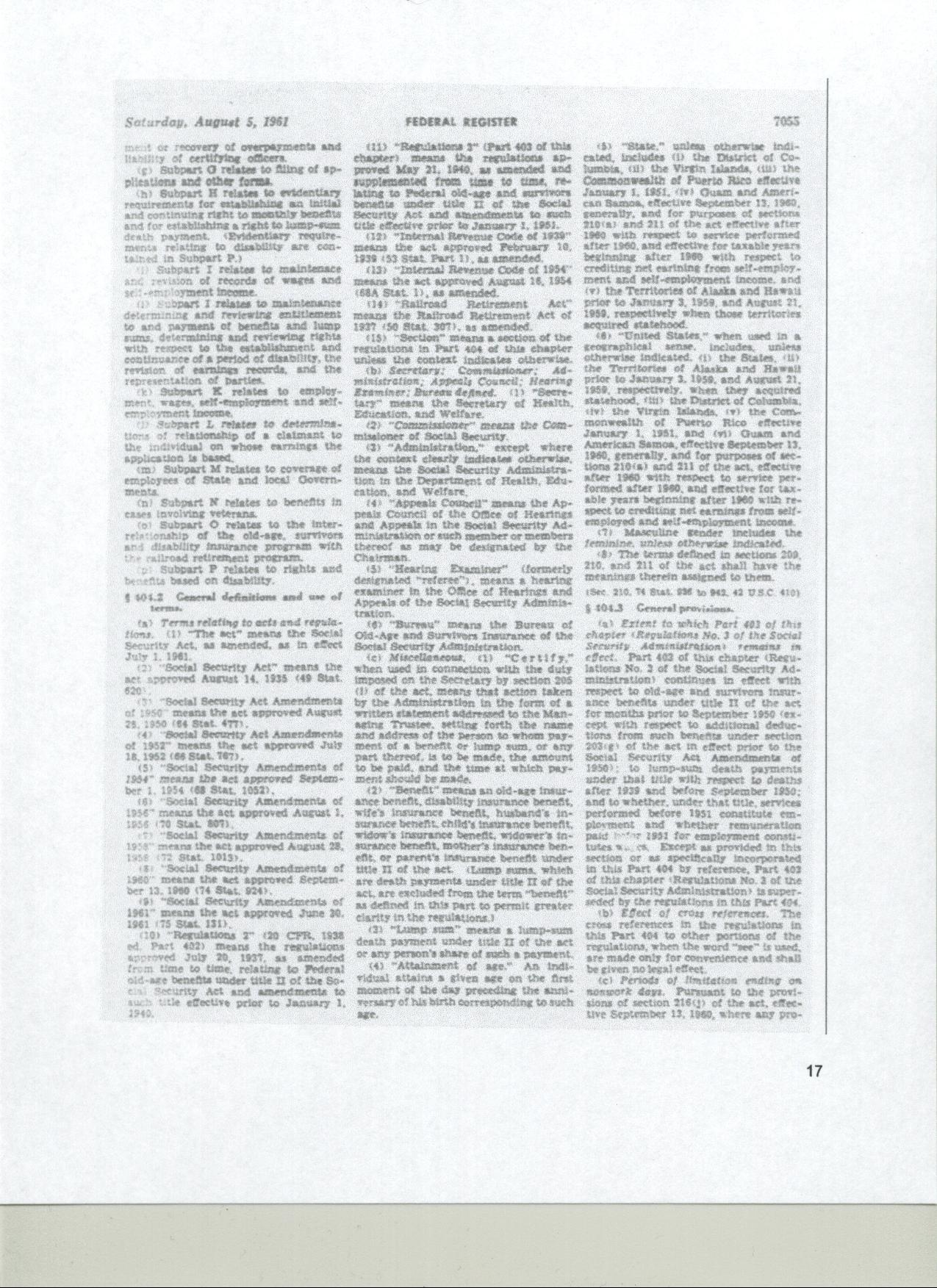

referring to the Federal Register entry at 26 FR 7055, Aug. 5, 1961 (shown on page 17) in the third

column it is noticed that in 404.2(c)(8) it states "The terms defined in sections 209, 210, and 211 of the

act shall have the meanings therein assigned to them". Section 209 of the Act is codified at Title 42

Section 409, therefore if an exemption exists for chapter 24 it also applies to chapter 21 (and 22).

This means that a look at chapter 24 section 3401 Definitions is in order. In 3401(a) Wages, the following

is stated:

"For purposes of this chapter, the term "wages" means all remuneration (other than fees paid to a public

official) for services performed by an employee for his employer, including the cash value of all

remuneration (including benefits) paid in any medium other than cash; except that such term shall not

include remuneration paid— "

In 3401(a)(8)(A) it states "for services for an employer (other than the United States or any agency

thereof)— " and in subsection (i) states "performed by a citizen of the United States if, at the time of the

payment of such remuneration, it is reasonable to believe that such remuneration will be excluded from

gross income under section 911.

The first thing noticed in this subsection is that the term "employee" was not used, it states "a citizen of

the United States. A look at IRC section 911 reveals that it in regards to an exclusion of a specific amount

of remuneration for U.S. citizens or residents thereof living abroad. Since a U.S. Citizen living within the 50

State Republics does not fall within the meaning of IRC section 911 they are exempt with no

remuneration while working in the private sector considered "wages" within the meaning of the term

defined. This is born out by Federal Register entry for 26 CFR section 31.3401(a)-1 at T.D. 6654, 28 FR

5251, May 28, 1963 shown on page 18 where it states for section 31.3401(a)-1:

(a) In general. (1) The term "wages'' means all remuneration for

services performed by an employee for his employer unless specifically

excepted under section 3401(a) or excepted under section 3402(e).

This has been shown to exist at IRC section 3401(a)(8)(A)(i).

The IRC sections and regulations are therefore in agreement with still standing decisions of the supreme

Court of the United States. In regards to the FICA and RRTA withholdings the following ruling applies:

"The catalogue of means and actions which might be imposed upon an employer in any business, tending to the

satisfaction and comfort of his employees, seems endless. Provision for free medical assistance, nursing,

clothing, food, housing, and education of children, and a hundred other matters might with equal propriety be

proposed as tending to relieve the employee of mental strain and worry. Can it fairly be said that the power of

Congress to regulate interstate commerce extends to the prescription of any or all of these things? It is not

apparent that they are really and essentially related solely to the social welfare of the worker, and therefore

remote from any regulation of commerce as such ? We think the answer is plain. These matters obviously lie

outside the orbit of congressional power". - Railroad Retirement Board v. Alton Railroad Co, 295 U.S. 330, 55

S. Ct. 758 (1935), [emphasis added]

It is now apparent that private sector employers are erroneously reporting remuneration as "wages" that

are not such within the meaning defined. Whether so done based on ignorance, faulted tax counsel, or by

direction and pressure it makes no difference, a violation of Constitutional Rights has occurred.

Another factor to look at is that the Forms prescribed pertain to reporting for "employees". This term is not

all encompassing and is limited to those stated as such in IRC section 3401(c) by using the definition of

"includes" and "including" given in IRC section 7701(c) per 26 CFR 301.7701-16 with Federal Register

authority at T.D. 7977, 49 FR 36836, Sept. 20, 1984.

Since the terms "wages" and "employee" are inter-dependent another look at the definition of "wages"

will add merit to what has been stated. Section 3401(c) defines an employee as : "For purposes of this

chapter, the term ''employee'' includes an officer, employee, or elected official of the United States, a

State

, or any political subdivision thereof, or the District of Columbia, or any agency or instrumentality ofany one or more of the foregoing. The term ''employee'' also includes an officer of a corporation."

Therefore, by applying the definition of "includes and including" in IRC section 7701(c) an employee is as

stated in IRC section 3401(c).

The regulations for enforcement are found in Sec. 31.3401(c)-1 Employee. In subsection 31.3401(c)-1(c)

an exclusion is made for those in an independent trade, business, or profession who offer their

services to the public sector: "Generally, physicians, lawyers, dentists, veterinarians, contractors,

subcontractors, public stenographers, auctioneers, and others who follow an independent trade, business, or

profession, in which they offer their services to the public, are not employees."

Additionally, 31.3401(c)-1(a) limits the application to certain classes of government employees: "The term

employee includes every individual performing services if the relationship between him and the person

for whom he performs such services is the legal relationship of employer and employee. The term

includes officers and employees, whether elected or appointed, of the United States, a State,

Territory, Puerto Rico, or any political subdivision thereof, or the District of Columbia, or any

agency or instrumentality of any one or more of the foregoing."

Notice the usage of the term "includes" and the words "elected" and "appointed". This limits the

designation as "employee" to only those that are elected to office, or appointed to a key position. It does

not include the clerks, janitors, or others plying a common trade and employed by the government. If you

are government employed and wish to determine if you are considered an "employee" refer to 5 U.S.C.

section 2105 Employee.

That the terms "individual" and "employee" are not always synonymous is shown in the regulations at 26

CFR Sec. 31.3401(a)-2 Exclusions from wages (Federal Register entries at T.D. 6516, 25 FR 13032,

Dec. 20, 1960, as amended by T.D. 6654, 28 FR 5251, May 28, 1963; T.D. 7096, 36 FR 5216, Mar. 18,

1971):

(a) In general. (1) The term "wages'' does not include any

remuneration for services performed by an employee for his employer

which is specifically excepted from wages under section 3401(a).

(2) The exception attaches to the remuneration for services

performed by an employee and not to the employee as an individual; that is,

the exception applies only to the remuneration in an excepted category.

Which states that an "employee" gets the exemptions only while in an excepted category of individuals.

One may be an "employee" and an "individual", but not all "individuals" are "employees".

Therefore the remuneration of those in government who are elected or appointed is what constitutes

"wages" for the purpose of Chapter 24 of the IRC (also Chapters 21 and 22 as previously shown). This is

in keeping with another court decision:

"An income tax is neither a property tax nor a tax on occupations of common right, but is an EXCISE tax ... The

legislature may declare as 'privileged' and tax as such for state revenue, those pursuits not matters of common

right, but it has no power to declare as a 'privilege' and tax for revenue purposes, occupations that are of

common right." - Simms v. Ahrens, 271 SW 720. [emphasis added]

This congress did, through implementation of the Buck Act (4 U.S.C. Sections 105-113). In Section

110(e), this Act authorized any department of the federal government to create a "Federal area" for

imposition of the "Public Salary Tax Act of 1939". This tax is imposed at 4 U.S.C.S. Sec. 111. The rest of

the taxing law is found in the Internal Revenue Code. The Social Security Board had already created a

"Federal area" overlay.

Again it is apparent that private sector employers are submitting erroneous forms in regards to taxation.

Not only are they reporting remuneration that does not constitute wages as such, they are also counting

employees who are not such by definitions in the IRC, their regulations, or in the Federal Register.

3. Title 26 (IRC) Section. 6012. General requirement of return, statement, or list

IRC section 6012(a) pertains to Returns with respect to income taxes under subtitle A and 6012(b)

pertains to Returns made by fiduciaries and receivers. For this reason section, 6012 does not apply and

there are no entries in the Federal Register giving it effect of law. They are not required as it has

previously been shown that Subtitle A does not apply to U.S. Citizens and Nationals living and working

within the 50 State Republics.

4. Title 26 (IRC) Section. 6020. Returns prepared for or executed by Secretary

IRC section 6020(b)(1) states "If any person fails to make any return required by any internal revenue law

or regulation made thereunder at the time prescribed therefore, or makes, willfully or otherwise, a false or

fraudulent return, the Secretary shall make such return from his own knowledge and from such

information as he can obtain through testimony or otherwise." Again, as was the case with IRC sections

6001 and 6011 this statement is vague in that it does not identify the taxes. However, through the

regulations for IRC sections 6001 and 6011 it has been determined just what information the IRS has a

right to ask for and the forms to be used. This can be verified by the wording in IRC section 6020 "any

return required by any internal revenue law or regulation made thereunder" as compared with that found

in IRC section 6011 "When required by regulations prescribed by the Secretary any person made liable

for any tax imposed by this title, or with respect to the collection thereof, shall make a return or statement

according to the forms and regulations prescribed by the Secretary". Therefore, the returns, as made by

the secretary are limited to those previously identified by the regulations for IRC sections 6001 and 6011.

This bears out that these sections (6001, 6011, and 6020) are in harmony and agreement.

In looking at the regulations for IRC section 6020 only one was noted, 301.6020-1 and it was noticed that

it has no entry into the Federal Register. However, it was located as called out in 27 CFR Parts 53 and

70. These parts are Manufacturers excise taxes -- firearms and ammunition and Procedure and

administration respectively. 27 CFR Part 53 is entered in the Federal Register with final rule status by T.D.

ATF-308, 56 FR 303, Jan. 3, 1991. For Part 70, it was originally located in Part 70.61 by T.D. ATF-251,

52 FR 19314, May 22, 1987 but relocated to Part 70.42 by T.D. ATF-301, 55 FR 47604, Nov. 14, 1990.

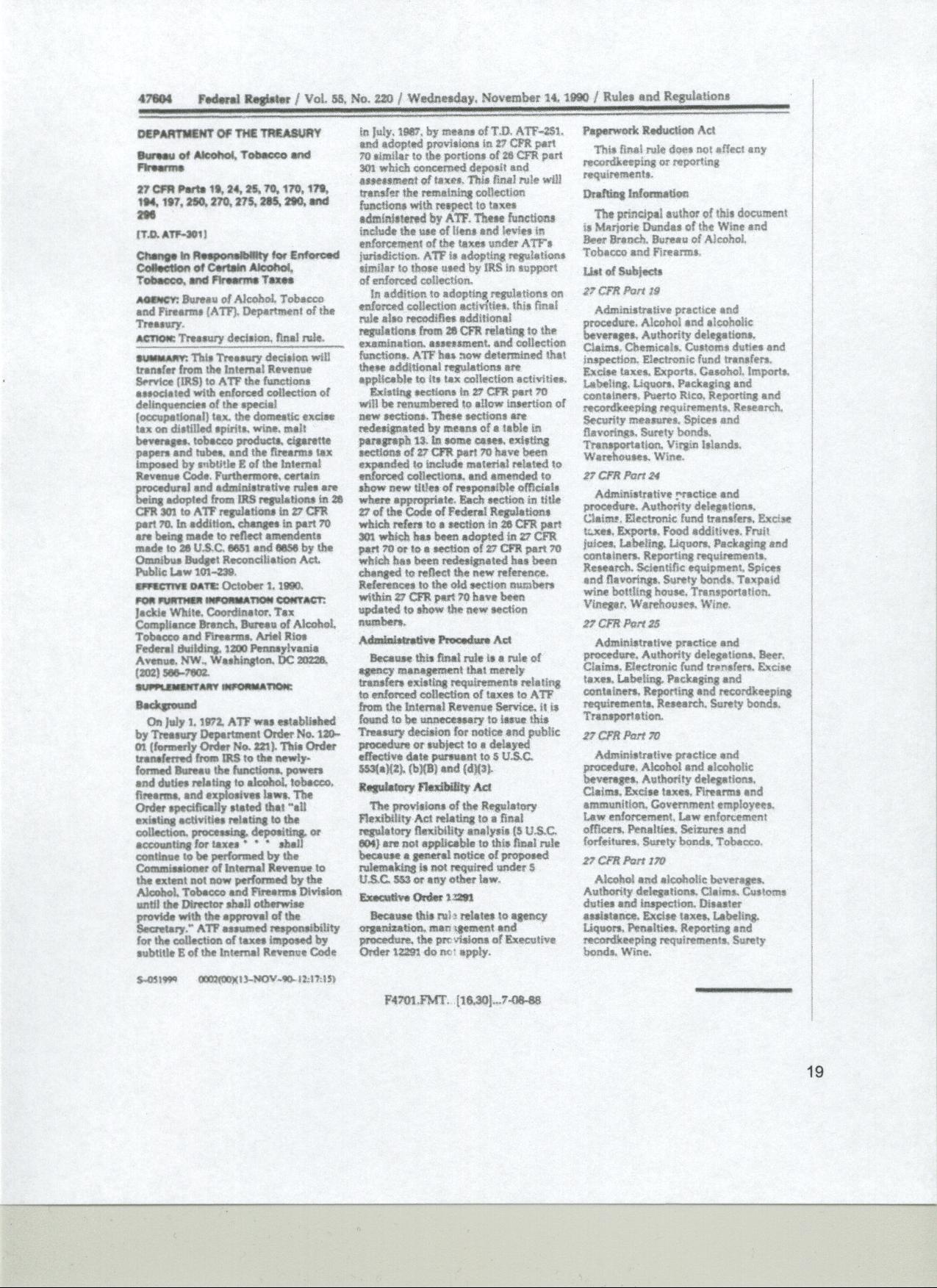

The Treasury Decision (T.D.) Federal Register entry at 55 FR 47604 is shown on page 19 of this file.

The page at T.D. ATF-301, 55 FR 47604, Nov. 14, 1990, as shown on page 19 has several important

facts indicated on it. The Summary and Background text gives in a very understandable form, the facts

concerning the take-over of tax functions by the BATF in regards to ATF taxable activities. In two places,

Administrative Procedure Act and Paperwork Reduction Act, it states the "final rule" status of T.D. ATF-

301. Since it is the Procedures and Administration part we are interested in, a look at the page at T.D.

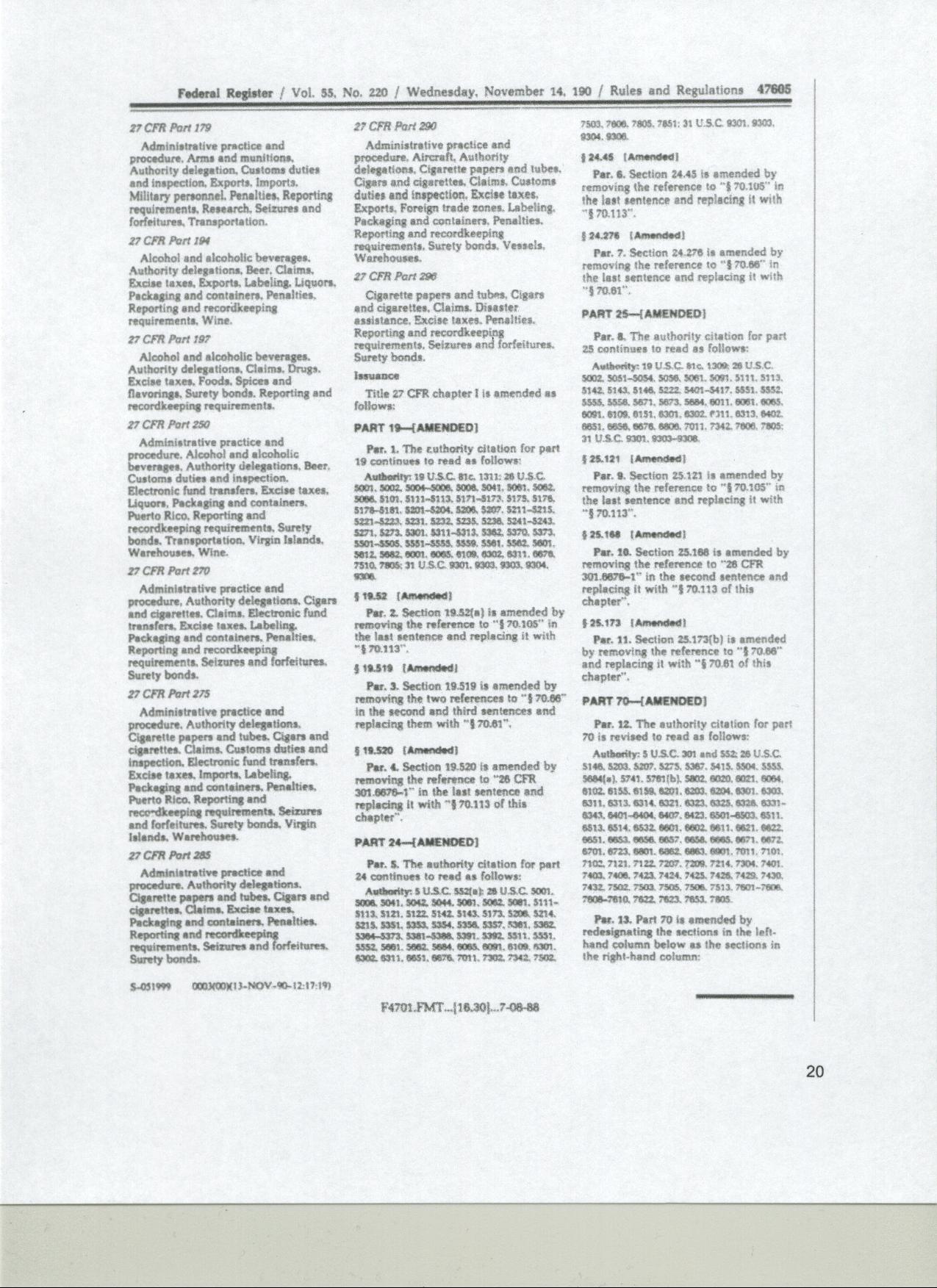

ATF-301, 55 FR 47605, Nov. 14, 1990 that we must look at. This page is shown on at the bottom of this file.

Located at the bottom of the third column as par. 12 the revised authority citation for Part 70 is given. It

should be noted that 26 U.S.C. section 6020 is listed. This is the only Federal Register entry for this

section that has final rule status giving it legal effect. Therefore, enforcement is by ATF regulated activity.

It is in regards to this section that the IRS establishes the base for accomplishing unlawful liens

and levies. Through their internal procedures they generate a "dummy substitute for return" against the Form

1040A (note that this form is not one authorized via IRC sections 6001 and 6011 and their regulations)

and enter it in the Individual Master File (IMF) of the individual(s) concerned.

The Internal Revenue Manual, though no law shows the IRS is aware that it is a "dummy SFR" in [104.3]

9.6 Substitutes for Return where it gives specific instructions for generating a SFR and in 1.1 states

"When preparing SFRs, the procedures listed below must be followed: Prepare a "dummy/SFR" for each

tax period." It then gives exact steps to be followed.

From the above it is plain to see that IRC section 6020 and its regulation apply only to ATF taxable

activities.

Further; according to the Internal Revenue Manual concerning what authority exists for implementing 6020(b) authority it states:

Internal Revenue Manual

Part 5

Collecting Process

Chapter 1

General

Section 11

Delinquent Return

Accounts

5.1.11.9 (05-27-1999)

IRC 6020(b) Authority

The

following returns may be prepared, signed and assessed under the authority of

IRC 6020(b):

A. Form 940, Employer's Annual Federal Unemployment

Tax Return

B. Form 941, Employer's Quarterly Federal Tax Return

C. Form 942, Employer's Quarterly Tax Return for Household Employees

D. Form 943, Employer's Annual Tax Return for Agricultural Employees

E. Form 720, Quarterly Federal Excise Tax Return

F. Form

2290, Heavy Vehicle Use Tax Return

G. Form CT-1, Employer's

Annual Railroad Retirement Tax Return

H. Form 1065, U.S. Partnership

Return of Income

The following are authorized to execute returns under IRC

6020(b):

A. Revenue officers.

B. Automated Collection System (ACS) and

Collection Support function (CSf) managers GS-9 and above.

5. Title 26 (IRC) Section. 6201. Assessment authority

Section 6201 of the IRC sets forth the assessment authorities. As was the case with IRC section 6020 a

single regulation exists, located at 301.6201-1. This regulation, like 301.6020-1 has no entry into the

Federal Register. However, it was located as called out in 27 CFR Part 70 Procedure and administration

(Part 70.42 with Federal Register entry at T.D. ATF-251, 52 FR 19314, May 22, 1987. Redesignated and

amended by T.D. ATF-301, 55 FR 47606 and 47610, Nov. 14, 1990). By referring to T.D. ATF-301, 55 FR

47605, Nov. 14, 1990 as shown on below it will be noted in the listing for Part 70.These are final rule

entries. Therefore, enforcement is by ATF regulated activity.

6. Title 26 (IRC) Section. 6203. Method of assessment

IRC section 6203 states "The assessment shall be made by recording the liability of the taxpayer in the

office of the Secretary in accordance with rules or regulations prescribed by the Secretary. Upon request

of the taxpayer, the Secretary shall furnish the taxpayer a copy of the record of the assessment.

26 CFR Sec. 301.6203-1 Method of assessment, details the stringent requirements in regards to an

assessment in that the assessment shall be made by an assessment officer signing the summary record

of assessment. The summary record, through supporting records, shall provide:

a) Identification of the taxpayer,

b) the character of the liability assessed,

c) the taxable period, if applicable, and

d) the amount of the assessment.

It further states that the date of the assessment is the date the summary record is signed by an

assessment officer.

It also explicitly states "If the taxpayer requests a copy of the record of assessment, he shall be furnished

a copy of the pertinent parts of the assessment which set forth the name of the taxpayer, the date of

assessment, the character of the liability assessed, the taxable period, if applicable, and the amounts

assessed.

However, the IRS uses the "dummy SFR" generated in IRC section 6020 to generate false assessments

against the "dummy SFRs" and input them into the Automated Information Management System (AIMS).

These assessments do not meet the requirements of IRC section 6203 or regulation at 301.6203-1 in that

they do not exist as required by regulation.

In this regard, numerous attempts at obtaining copies of the 1040A "dummy return assessments as

entered in Individual Master Files have been ignored, delayed under faulted excuses, or attempted to be

satisfied by a RACS Report 006 that fails to meet the requirements of 26 CFR section 301.6203-1, or of

27 CFR Part 70.71 where authority has been placed by Federal Register entry at T.D. ATF-301, 55 FR

47611, Nov. 14, 1990. Again, by referring to T.D. ATF-301, 55 FR 47605, Nov. 14, 1990 as shown on

page 20 of this transmittal you will see 26 USC section 6203 listed under the authority citation for Part 70.

In regards to the failure of the IRS to provide copies of the assessments, I offer the following court

findings:

Upon request, FOIA mandates disclosure of records held by a federal agency, see 5 U.S.C. § 552

unless the documents fall within enumerated exemptions, see §552(b). "[T]hese limited exemptions do

not obscure the basic policy that disclosure, not secrecy, is the dominant objective of the Act,"

Department of Air Force v. Rose, 425 U.S. 352, 361 (1976); "[c]onsistent with the Act’s goal of broad

disclosure, these exemptions have been consistently given a narrow compass," Department of Justice

v. Tax Analysts, 492 U.S. 136, 151 (1989); see also FBI v. Abramson, 456 U.S. 615, 630 (1982) ("FOIA

exemptions are to be narrowly construed").

The point is not to protect Government secrecy pure and simple, however, and the first condition of

Exemption 5 is no less important than the second; the communication must be "inter-agency or intraagency."

5 U.S.C. § 552(b)(5). Statutory definitions underscore the apparent plainness of this text. With

exceptions not relevant here, "agency" means "each authority of the Government of the United States,"

§551(1), and "includes any executive department, military department, Government corporation,

Government controlled corporation, or other establishment in the executive branch of the Government .

. ., or any independent regulatory agency," §552(f). - Department of the Interior and Bureau of Indian

Affairs, Petitioners v. Klamath Water Users Protective Association on Writ of Certiorari to the United

States Court Of Appeals for the Ninth Circuit [March 5, 2001]

That the IRS is well aware that a lawfully completed Summary of Assessment must exist is shown within

their Internal Revenue Manual:

3.17.63.14.4

(10-01-2001)Account 6110 Withholding Tax Assessments--Principal

1. This account is used to summarize the total amounts of assessments of tax class 1

Principal as provided by the Internal Revenue Code. The balance of this account represents total tax class 1 Principal assessments for the year.2. All

principal assessments must be recorded on Summary Record of Assessments (Assessment Certificate). The Assessment Certificate is the legal document that permits collection activity.3. Total tax class 1 assessments for the month will be summarized on computer generated Form 2162 which

will become the external subsidiary.

3.17.63.14.5

(10-01-2001)Account 6111 Withholding Tax Assessments--Penalty

1. This account is used to summarize the total amounts of assessments of tax class 1

Penalties as provided by the Internal Revenue Code. The balance of this account represents total tax class 1 penalty assessments for the year.2. All

penalty assessments must be recorded on summary Record of Assessments (Assessment Certificate).The Assessment Certificate is the legal document that permits collection activity.

3. Total tax class 1 assessments for the month will be summarized on computer generated Form 2162 which will become the external subsidiary.

3.17.63.14.6

(10-01-2001)Account 6112 Withholding Tax Assessments--Interest

1. This account is used to summarize the total amounts of assessments of tax class 1

Interest as provided by 12 the Internal Revenue Code. The balance of this account represents total tax class 1 interest assessments for the year.2. All

interest assessments must be recorded on Summary Record of Assessments (Assessment Certificate).The Assessment Certificate is the legal document that permits collection activity.

3. Total tax class 1 assessments for the month will be summarized on computer generated Form 2162 which will become the external subsidiary.

3.17.63.14.7

(10-01-2001)Account 6120 Individual Income Tax Assessments--Principal

1. This account is used to summarize the total amounts of assessments of tax class 2

Principal as provided by the Internal Revenue Code. The balance of this account represents total tax class 2 principal assessments for the year.2. All

principal assessments must be recorded on Summary Record of Assessments (Assessment Certificate). The Assessment Certificate is the legal document that permits collection activity.3. Total tax class 2 assessments for the month will be summarized on computer generated Form 2162 which will become the external subsidiary.

3.17.63.14.8

(10-01-2001)Account 6121 Individual Income Tax Assessments--Penalty

1. This account is used to summarize the total amounts of assessments of tax class 2

Penalties as provided by the Internal Revenue Code. The balance of this account represents total tax class 2 penalty assessments for the year.2. All

penalty assessments must be recorded on Summary Record of Assessments (Assessment Certificate).The Assessment Certificate is the legal document that permits collection activity.

3. Total tax class 2 assessments for the month will be summarized on computer generated Form 2162 which

will become the external subsidiary.

Note Item 2 in all the above IRM sections: "

All principal (or penalty/interest) assessments must be recorded on Summary Record of Assessments (Assessment Certificate). The Assessment Certificate is the legal document that permits collection activity."7. Title 26 (IRC) Section. 6301. Collection authority

As before, this section has but one regulatory entry (301.6301-1) having no shown Federal Register entry. As

stated previously the final rule regulatory authority is found in 27 CFR Part 70 Procedure and administration

Parts 70.11 Meaning of terms, 70.51 Collection authority, and 70.65 Use of commercial banks. The entry at

Part 70.51 is found in the Federal Register in final rule status at T.D. ATF-301, 55 FR 47611, Nov. 14, 1990.

By referring to T.D. ATF-301, 55 FR 47605, Nov. 14, 1990 as shown on page 20 it will be noted in the listing

for Part 70. Again, this activity does not apply to those not engaged in ATF taxable activities.

8. Title 26 (IRC) Section 6321 Lien for tax Section 6321 reads "If any person liable to pay any tax neglects or

refuses to pay the same after demand, the amount (including any interest, additional amount, addition to tax,

or assessable penalty, together with any costs that may accrue in addition thereto) shall be a lien in favor of

the United States upon all property and rights to property, whether real or personal, belonging to such

person."

Under Short Title it states: "Pub. L. 89-719, Sec. 1(a), Nov. 2, 1966, 80 Stat. 1125, provided that: ``This Act

[enacting sections 3505, 7425, 7426, and 7810 of this title, amending sections 545, 6322 to 6325, 6331,

6332, 6334, 6335, 6337 to 6339, 6342, 6343, 6502, 6503, 6532, 7402, 7403, 7421, 7424, 7505, 7506, and

7809 of this title, sections 1346, 1402, and 2410 of Title 28, Judiciary and Judicial Procedure, and section

270a of Title 40, Public Buildings, Property, and Works, redesignating section 7425 as 7427 of this title, and

enacting provisions set out as notes under sections 6323 and 7424 of this title, and under section 1346 of

Title 28] may be cited as the `Federal Tax Lien Act of 1966'.''

Of the sections in the IRC listed, the following have governing authority in 27CFR Part 70: 6323, 6325,

6331, 6332, 6334, 6335, 6337 to 6339, 6342, 6343, 6502, 6503, 6532, 7403, 7424, 7425, 7426, 7505,

7506, 7809 and 7810 (refer to T.D. ATF-301, 55 FR 47605, Nov. 14, 1990 shown on page 20). Section

6325 also has regulations located in 26 CFR Part 401, which is Temporary procedures and administration

regulations under the Tax Equity and Fiscal Responsibility Act of 1982 (Pub. L. 97-248). A single regulation

is listed in 26 CFR Part 401, being 401.6325-1 Release of liens with Federal Register entry at T.D. 7886, 48

FR 17069, Apr. 21, 1983; 48 FR 19878, May 3, 1983. The location of section 7403 regulations in 27 CFR

Part 70 is of particular importance for it specifies the action to enforce lien or to subject property to

payment of tax.

This leaves the following sections:

a) 545 - Undistributed personal holding company income

b) 3505 - Liability of third parties paying or providing for wages

c) 6324 - Special liens for estate and gift taxes

d) 7402 - Jurisdiction of district courts

e) 7421 - Prohibition of suits to restrain assessment or collection

f) 7809 - Deposit of collections

g) 7810 - Revolving fund for redemption of real property

None of the above (a) through (g) have final rule/regulation entered in the Federal Register, leaving them

without legal effect within the 50 State Republics. Therefore, enforcement of Lien for Taxes provisions are

governed explicitly through the authority of 27 CFR Part 70.141 Lien for taxes. Here it states "If any

person liable to pay any tax under provisions of 26 U.S.C. enforced and administered by the Bureau

neglects or refuses to pay the same after demand, the amount (including any interest, additional amount,

addition to tax, or assessable penalty, together with any costs that may accrue in addition thereto) shall

be a lien in favor of the United States upon all property and rights to property, whether real or personal,

tangible or intangible, belonging to such person". The words to note are "under provisions of 26 U.S.C.

enforced and administered by the Bureau" meaning enforcement is by BATF authority.

It has been common practice for IRS agents, apparently with the blessing and assistance of supervisory

personnel to use the "dummy SFRs entered in the Individual Master File (refer to Item 4 - Title 26 (IRC)

Section. 6020. Returns prepared for or executed by Secretary on page 9) and issue/file Notices of Lien

without having authority (IRC section 6201 - refer to Item 5 on page 10) or an assessment of legal effect

per IRC Section. 6203. Method of assessment (refer to Item 6 on page 10, and without authority (refer to

Title 26 (IRC) Section. 6301. Collection authority on page 12). 9. Title 26 (IRC) Section 6331 Levy and

distraint

Title 26 (IRC) Section 6331 Levy and distraint reads in subsection (a) who levy can be made upon: "Levy

may be made upon the accrued salary or wages of any officer, employee, or elected official, of the United

States, the District of Columbia, or any agency or instrumentality of the United States or the District of

Columbia". This is a definite statement and is backed by the authoritative regulation found in 27 CFR Part

70.161(a)(4)(i) (refer to T.D. ATF-301, 55 FR 47605, Nov. 14, 1990 as shown on page 20), which is

further reinforced by the meaning given the term "employer in 70.161(a)(4)(i)(A) and (B):

(A) The officer or employee of the United States, the District of

Columbia, or of the agency or instrumentality of the United States or

the District of Columbia, who has control of the payment of the wages,

or

(B) Any other officer or employee designated by the head of the

branch, department, or agency, or instrumentality of the United States

or of the District of Columbia as the party upon whom service of the

notice of levy may be made.

It should be noted that 27 CFR Part 70.161(a)(4) lists others subject to levy on "wages" and does not

include an U.S. Citizen, or national living and working within the 50 State Republics.

As was stated in regards to liens, it has been common practice for IRS personnel to issue Notices of Levy

based on the "dummy SFRs without having authority (sections 6201 and 6301) and without proper

assessments (section 6203).

10. Title 26 (IRC) Section. 6682. False information with respect to withholding

It is to be noted that this section of the IRC has no regulatory entries in the Federal Register, therefore it

has no legal effect and not enforceable in regards to U.S. Citizens working and living within the 50 State

Republics. It is well known that U.S. companies, either being unaware of the definition of "wages" within

the IRC, or taking advice from faulted counsel, or bowing to threats and pressure from the IRS demand a

W-4 Form from all and therefore normally report remuneration as "wages" which are not such within the

meaning of IRC section 3401(a)(8)(A)(i) with regulations at 26 CFR section 31.3401-1 and IRC section

3121 and Title 42 section 409 with regulations at 20CFR section 404.2

There exists the possibility that the IRS, being fully aware that a W-4 Form is not required of all are

treating those demanded as "voluntary W-4 Forms under IRC section 3402.

Without authority having legal effect this section is unenforceable against U.S. Citizens living and working

within the 50 Sovereign Republics for private sector employers. Still, the IRS offices issue penalties

unlawfully using this section as their authority to do so.

The Notice of Liens and Levies issued by the IRS are not accompanied by a valid assessment and the IRS

has been unable to provide any under the FOIA that meet the lawful requirements of IRC section 6203. They

do not exist. The need for such has been recognized in the courts, the following cases are two that the IRS is

very aware of since it appears within their IRM and training material:

"Plaintiff relies heavily on Brafman v. United States, 384 F.2d 863 (5

th Cir. 1967), where an assessment wasinvalidated due to the lack of a signature on the 23C Form. This defect, however, was a significant violation of

the regulation…

… A signature requirement protects the taxpayer by ensuring that a responsible officer has approved the

assessment… " -

Curley v. U.S. 791 F. Supp 52 (E.D.N.Y. 1992) Cite as 764 FEDERAL SUPPLEMENTPage 315

"… However, there is no indication in the record before us that the "Summary Report of Assessments", known as

Form 23C, was completed and signed by the assessment officer as required by 26 CFR

§ 301.6203-1.3 Nor dothe Certificates of Assessments and Payments contain 23C dates which would allow us to conclude that a Form

23C form was signed on that date. See United States v. Dixon, 672 F. Supp. 503, 505-506 (M.D.Ala.1987). Thus

we find that the plaintiff has raised a factual question concerning whether IRS procedures were followed in

making the assessments…

This regulation provides, in relevant part, that "[t]he assessment shall be made by an assessment officer

signing the summary record of assessment… " – Brewer v. U.S. 764 F. Supp. 309 (S.D.N.Y. 1991)

11. Title 26 (IRC) Section. 7608. Authority of internal revenue enforcement officers

This section of the IRC is abused at will by IRS agents. The only final rule authorities giving legal effect

are found in 27 CFR Parts 70 (Procedure and administration), 170 (Miscellaneous regulations relating to

liquor), and 296 (Miscellaneous regulations relating to tobacco products and cigarette papers and tubes).

Concentration will be on 27 CFR Part 70, subpart 33 as parts 170 and 296 apply only to those involved in

such activities.

In 70.33, Authority of enforcement officers of the Bureau it gives the following authorities to "Any special

agent or other officer of the Bureau by whatever term designated, whom the Director or a special agent in

charge charges with the duty of enforcing any of the criminal, seizure, or forfeiture provisions of the laws

administered and enforced by the Bureau pertaining to commodities subject to regulation by the Bureau,

the enforcement of which such officers are responsible, may perform the following functions

a) Carry firearms;

b) Execute and serve search warrants and arrest warrants, and serve subpoenas and

summonses issued under authority of the United States;

c) In respect to the performance of such duty, make arrests without warrant for any offense

against the United States committed in his presence, or for any felony cognizable under the

laws of the United States if he has reasonable grounds to believe that the person to be

arrested has committed, or is committing, such felony; and

d) In respect to the performance of such duty, make seizures of property subject to forfeiture to

the United States.

The wording "to "Any special agent or other officer of the Bureau" and "enforcing any of the criminal,

seizure, or forfeiture provisions of the laws administered and enforced by the Bureau" limit activity to the

BATF not the IRS. 27 CFR Part 70.33 was entered in the Federal Register at T.D. ATF-6, 38 FR 32445,

Nov. 26, 1973 as Part 70.28 (refer to page ?). In 1978 it was amended by T.D. ATF-48, 43 FR 13531,

Mar. 31, 1978. Redesignated by T.D. ATF-301, 55 FR 47606, Nov. 14, 1990 (Note: The use of the word

"Bureau" instead of "agency" in 26CFR601.101)

The abuses as given above indicate a deliberate and well planned theft of property by the IRS. Since it

followed an orderly path of violations it cannot be considered "accidental" or by "mistake". All actions are

inter-related and done deliberately. These acts are criminal in nature and may even be considered as treason

and conspiracy to commit treason.

Unfortunately, congress has given no remedies to U.S. Citizens. The remedies, Tax Court or District Court

are Article 1 Courts having territorial jurisdiction only. As the tax on income (Subtitle A) applies to taxpayers

residing or doing business abroad, foreign taxpayers deriving income from sources within the United States,

and taxpayers who are required to withhold tax on certain payments to nonresident aliens and foreign

corporations these remedies are appropriate. However, by petitioning the tax court, or making a plea or

presenting arguments in a U.S. District Court a U.S. Citizen grants them jurisdiction. In these courts,

particularly since the invocation of Treasury/IRS 46.002 it is a rarity to get to present the evidence of the tax

laws, or present knowledgeable witnesses. You are denied due process of law and judged on dicta.

Treasury/IRS 46.002 is the instrument by which the IRS-CID is tasked to monitor the performance of Article 1

court judges and U.S. Attorneys. This makes them subject to IRS harassment and threats, and even hints at

the possibility of "rewards based on performance".

The Tax Advocates and TIGTA are of no recourse either. They themselves are part of the fraudulent scheme,

misrepresenting what the Supreme Court has stated in regards to the 16

th Amendment, and offering nothingbut the recourse to courts of no true jurisdiction.

Congress, in Public Laws 105-206 Sec. 1203 gave guidance for Termination of Employment for Misconduct

which stated "Subject to subsection (c), the Commissioner of Internal Revenue shall terminate the

employment of any employee of the Internal Revenue Service if there is a final administrative or judicial

determination that such employee committed any act or omission described under subsection (b) in the

performance of the employee's official duties. Such termination shall be a removal for cause on charges of

misconduct." This is set out as a note in IRC section 7804. However, subsection (c) gives the commissioner

the choice of other action, therefore destroying the purpose of the Public Law as stated. It accomplished

nothing. Additionally, Public Law 107-67, sec. 803 further weakened and destroyed any true meaning by

changing the wording in the note to "may" in place of "shall". This note has regulatory final rule authority in 26

CFR Part 801.

In the Hearing Before the Subcommittee On Treasury, Postal Service and General Government Committee

On Appropriations U.S. House Of Representatives on March 21, 2001 the TIGTA stated that it needed to

continue to focus on rights by:

a) Restricting the use of enforcement statistics to evaluate IRS employees.

b) Not designating taxpayers as illegal tax protesters. (protester of an illegal tax?)

c) Providing proper and timely notice that a federal tax lien has been filed.

d) Not withholding information in response to taxpayers’ written requests for information under the

Freedom of Information Act of 1988 or the Privacy Act of 1974.

By their actions, as previously stated in this transmission they have lost their focus and continue to allow the

filing of liens and levies without proper assessments and continue to allow the withholding of information

under the Freedom of Information Act of 1988 or the Privacy Act of 1974.

There is no evidence that TIGTA, or the IRS feel compelled to fully comply with the Restructuring Act or to

redress personnel that routinely violate the Internal Revenue Laws, their regulations, the decision documents

of their own agencies, and the provisions of Title 5--Government Organization and Employees, Part I--The

Agencies Generally, Chapter 5--Administrative Procedure, Subchapter II--Administrative Procedure. They

operate with a feeling of impunity and not accountable for their fraudulent actions.

There is one saving section whereby a district director, service center director, or compliance center director

(director) can right the wrongs of these errant agents, that being IRC section 6343, whose regulations at 26

CFR 301.6343-1 and 301.6343-2 with final rule authority at T.D. 8587, 59 FR 35, Jan. 3, 1995.

If that is not done, then the federal government itself would be negligent if these agents were not charged

with violations of the Ethics in Government Act with authority at 27 CFR Part 70.333 (refer to T.D. ATF-301,

55 FR 47605, Nov. 14, 1990 shown on page 20); and at 5 CFR Part 3101 sourced at 60 FR 22251, May 5,

1995. These agents have operated under color of law and demanded, through fraudulent actions taxes that

are not even owed.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}